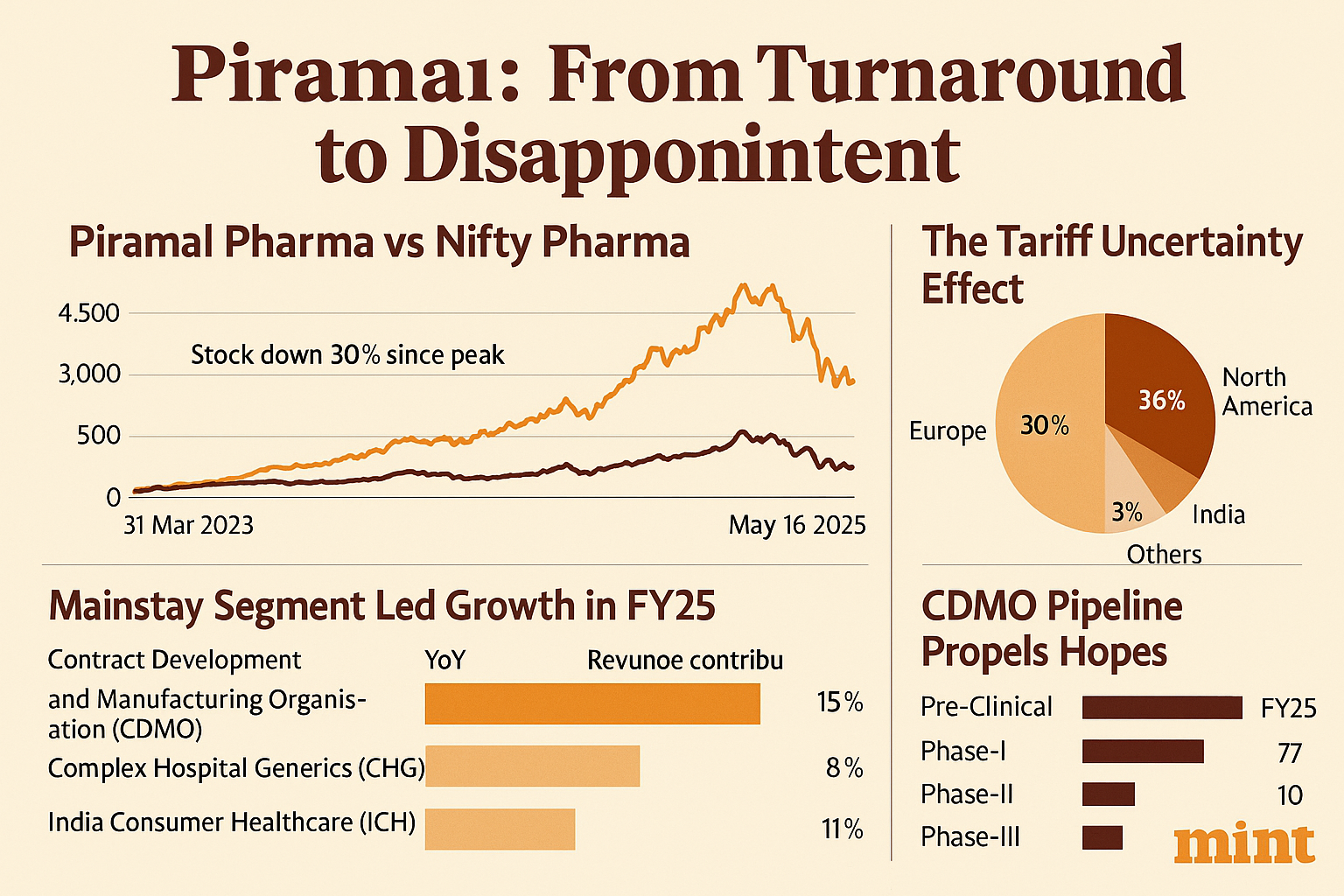

Mumbai-based Piramal Pharma Ltd (PPL) has captured the imagination of Indian equity investors with a turnaround story worthy of boardroom folklore. Since FY23, the pharmaceutical major more than tripled investor wealth, a feat that firmly positioned it ahead of the broader Nifty Pharma index. Yet, just as confidence peaked, a disappointing fourth quarter in FY25 reversed fortunes, with the stock shedding 30% from its November peak. The sudden correction has sparked a key question—is this a buying opportunity or a harbinger of deeper troubles?

The Turnaround: A Financial Renaissance

Between FY23 and FY25, PPL exhibited a compelling transformation:

Revenue CAGR: 14%

EBITDA Margin Expansion: From 12% to 17%

Net Profit Swing: From a ₹186 crore loss to a ₹91 crore profit

Debt Moderation: Net debt/EBITDA dropped from 5.6x to 2.7x

This recovery was underpinned by operational excellence and aggressive debt control, highlighting management’s focused execution.

Q4 FY25: A Reality Check

However, recent quarterly results threw cold water on investor enthusiasm:

Revenue Growth: Sluggish at 8% YoY

EBITDA Margin: Flat at 22%

Profit Growth: 52%, but inflated due to a base quarter write-off

Despite full-year progress, the muted growth and absence of margin expansion unsettled market sentiment, especially amid a broader climate of global uncertainty.

Segment Performance: CDMO at the Helm

PPL’s business comprises three key segments:

Segment

Revenue Share (FY25)

YoY Growth

CDMO (Contract Development and Manufacturing)

59%

15%

CHG (Complex Hospital Generics)

29%

8%

ICH (India Consumer Healthcare)

12%

11%

CDMO remained the linchpin, with growing exposure to on-patent commercial manufacturing and innovation work. Yet, rising costs and suboptimal overseas facility utilization have dented its operating leverage.

External Challenges: Tariffs and Drug Pricing Risks

Two major US policy overhangs threaten to reshape the playing field:

Tariff Uncertainty: Reciprocal tariffs could strip pharma of current exemptions, forcing Indian companies to consider costlier US-based production.

Trump’s Drug Pricing Order: This directive could curb pricing flexibility for on-patent drugs, undermining profitability.

Piramal derives over 36% of its revenue from North America, making it vulnerable. While it has invested $470 million in US facilities, additional $90 million in capex is underway, reflecting both risk and opportunity.

Customer Risk and Capacity Woes

PPL’s CDMO segment is heavily reliant on:

Top 10 Customers: Nearly 50% of CDMO revenue

Generic Exposure: Only 39%

Such concentration, coupled with tepid biotech funding in the US and delayed order cycles, has reduced utilization and operating efficiency. Growth for CDMO in FY26 is expected to slow to single digits.

Bright Spots: India Consumer Healthcare and CHG Potential

India remains a pillar of strength:

ICH Business: Crossed ₹1,000 crore in revenue

Growth Drivers: 52 new products, 49% revenue from strong brands, 39% e-commerce growth

CHG Segment saw subdued growth due to one-off expenses, but expansion efforts are expected to bear fruit starting FY26. Piramal continues to dominate:

Intrathecal Therapy: 75% US market share

Inhaled Anesthetics (Sevoflurane): 44% share

A robust product pipeline, including a psychiatric injectable and neonatal drug ‘Neoatricon,’ indicates future growth potential. Target for CHG: $600 million by FY30.

CDMO Pipeline and Strategic Tailwinds

Despite recent softness, the CDMO pipeline is promising:

Development Pipeline: 52 in FY17 → 145 in FY25

Targeted Growth: $1.2 billion revenue by FY30

Capex Plans: Focus on ADCs and injectables (a $20 billion market by 2028)

A potential US Biosecure Act may further boost Indian CDMOs by banning Chinese biotech imports—a strategic windfall for players like Piramal.

Volatility Alert: F&O contracts to be introduced soon

Management retains its FY30 vision of $2 billion revenue, 25% EBITDA margin, and 1x net debt/EBITDA, reinforcing long-term confidence.

Bottom Line

Piramal Pharma’s recent dip is a cocktail of cyclical headwinds and structural adjustments, not a derailment of its long-term growth thesis. Its diversified segmental strength, strategic capital allocation, and innovation-led CDMO push provide a solid foundation. Yet, tariff risks, customer concentration, and near-term margin pressures cloud the outlook.

For discerning investors, this could be a volatile yet potentially rewarding bet—if they have the patience to wait out the near-term storm.